Balancing the R&D equation: Measuring the return from pharmaceutical innovation

pharmafile | September 8, 2017 | News story | Medical Communications, Research and Development |

Following Deloitte’s anaylsis of the return on R&D spend by biopharmaceutical companies, this report reveals the key difficulties faced, as well as how approaches during drug development can boost the success of an asset.

This year our core quantitative analysis was supplemented with insights obtained through a number of qualitative interviews with industry executives and leading experts focussing on two key themes:

- Strategies employed by pharmaceutical companies during drug development that can positively influence the commercial success of an asset

- The approaches used to drive greater R&D efficiency, reversing the diseconomies of scale associated with drug development

Headline results

In 2016, the forecast returns generated by the original cohort declined to a low of 3.7 per cent, down from a high of 10.1 per cent in 2010 when our analysis started. To put this into context, the average industry cost of capital, the level against which R&D returns should be appraised, stands at roughly 8.4 per cent – almost five percentage points higher than the 2016 figure for the original cohort.

Despite the decline in returns, the original cohort has been very successful at commercialising their collective late-stage pipelines, launching 233 assets since 2010 with forecast lifetime sales of $1,538 billion. However, on launching an asset its value is transferred into the commercial portfolio, and companies are struggling to bring forward new assets into their late-stage pipelines to replace the value lost from those that are approved.

In our 2015 report, the extension cohort outperformed the original cohort on every measure, and while it is still out-performing the original cohort, in 2016 it experienced a decline in its overall performance. Static returns for the extension cohort fell from 16.1 per cent in 2015 to 9.9 per cent in 2016, with roughly half of this 6.2 percentage point decrease attributable to a strong year of commercialisation, with the successful launch of nine assets with total forecast sales of $187 billion.

Around half of the decrease in returns appears to be due to net commercialisation, but the rest is attributable to increasing R&D costs. While the decline in returns may be a reflection of natural volatility associated with the extension cohort’s collective pipeline size, alternatively, it may be that the extension cohort is starting to experience similar problems to the original cohort.

Asset sales are a long way from blockbuster levels

Forecast asset sales continue to decline, with average peak sales for the original cohort dropping to $394 million in 2016 – an 11.4 per cent year-on-year decrease since 2010. The extension cohort continues to outperform the original cohort despite a 28 per cent fall in forecast peak sales since 2015. Forecast average peak sales per asset for the extension cohort of $801 million in 2016 are over twice the amount forecast for the original cohort.

Within the product portfolio of the original cohort, there remains a wide range in forecast peak sales per asset. While there are a number of assets in the portfolio with high average peak sales, the curve for 2016 lags behind previous years with regards to aggregate peak sales. In 2010, 68 per cent of forecast peak sales came from blockbuster assets (those with risk-adjusted forecast peak sales above $1 billion), compared with 44 per cent in 2016. Furthermore, in 2010, 28 per cent of assets would have been considered to be blockbusters, compared to just 12 per cent in 2016.

R&D costs remain at blockbuster levels

Since 2015 there has been a slight decrease in the average cost to bring an asset from discovery to launch; however, the cost is still extremely high at $1,539 million – 30 per cent higher than the cost in 2010. While the original cohort’s costs have stabilised, the extension cohort has seen a significant increase in the average cost of bringing an asset from discovery to launch, to just below $2 billion in 2016, up from $1.26 billion in 2015 – a 57 per cent increase.

With R&D costs at blockbuster levels, and peak sales far from blockbuster status, we are left with an equation which does not add up for long-term stakeholder value, hence the strapline to this year’s report ‘Balancing the R&D equation’.

The shifting balance between sales from internally and externally-sourced assets

The original cohort is now less reliant on externally-innovated assets (those acquired through acquisitions, joint ventures or in-licensing) to drive forecast sales than it is on self-originated assets. In 2016, for the first time, forecast sales from external sources dropped below 50 per cent, to 43 per cent. M&A cycles play a large part in this trend. Industry consolidation in the late 2000s saw acquisitions bring significant value to the original cohort, however, the extent of integration is now at the point where new pipeline assets are synonymous with internal innovation.

While 2016 saw a reduction in the proportion of the extension cohort’s forecast late-stage pipeline value sourced externally (45 per cent in 2016 compared to 79 per cent in 2015), they still pursued an external innovation strategy through M&A, with three of the four companies making major acquisitions during this period.

Companies in the original cohort are struggling to maintain the value of their late-stage pipelines through progression of self-originated assets from earlier stages of development, meaning they are now likely to start reconsidering the risk-reward profile associated with external pools of innovation in order to reload their late-stage pipelines. This may well drive M&A activity in the coming years.

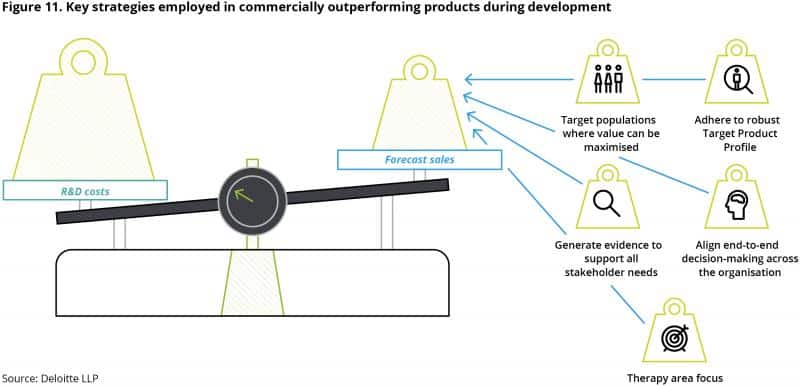

Balancing the R&D equation: Increasing pipeline value

Our research confirmed that there are key strategic choices being made throughout development that can be either accretive or destructive to an asset’s long-term value. These choices include decisions relating to therapeutic area (TA) focus, product strategy and designing a value-driven R&D programme.

TA focus

The original cohort of 12 companies vary in both size and focus, and forecast peak sales per asset continue to correlate with lower TA volatility. Our analysis again suggests that focussing on a detailed understanding of a disease state or mechanism of action within a TA – ‘pursuing the science’ – could offer higher rewards than following diseases or TAs for which drugs with significant sales already exist or where there is perceived to be a significant opportunity for sales – ‘pursuing the market’. Industry leaders interviewed by Deloitte confirmed that in-depth TA knowledge allows organisations to make better decisions about where to place their bets, and which products to kill early. The ability to leverage established relationships with key stakeholders throughout development, including academics, key opinion leaders, clinical investigators and patient advocacy groups, was also highlighted.

Product strategy

In order to develop a successful product strategy, organisations need to make critical decisions about indication approach, patient populations and positioning relative to the current standard of care.

A targeted indication strategy was highlighted by interviewees, who emphasised the importance of first indication at launch and the bearing that this has on the overall success of the product, particularly in striking the right balance between quickest approval, greatest uptake, and potential for premium pricing. Following a decision on disease area, organisations then face a choice regarding patient segmentation – whether to pursue a broad or targeted population? Sub-population targeting could expedite time to market, and increase the likelihood of clinical success and reimbursement. Finally, the product strategy needs to take into account existing treatment paradigms, ensuring clear differentiation from current, and future treatment options, in order to ensure reimbursement.

R&D programme design

Following selection of disease area, indication and patient population, the next stage where value can be added is the R&D programme design. Programme design begins with developing the detailed Target Product Profile (TPP), including both clinical and value-related endpoints, and establishing the discipline to stay committed to the key criteria. Early engagement with both regulators and payers can aid in refining critical endpoints. Endpoints enabling market access should be central to the development plan and a robust health economics and outcomes research (HEOR) strategy can demonstrate value to payers, providers and patients, and maximise commercial potential.

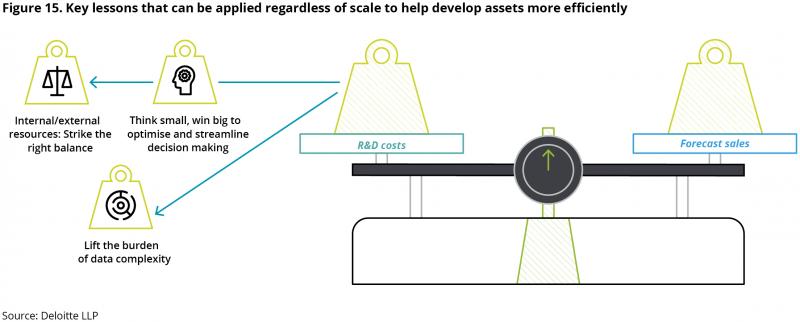

Balancing the R&D equation: Reducing the cost to launch

Our interviews with R&D leaders outlined some of the lessons learned across the areas of governance and decision-making, staffing and outsourcing, and dealing with data complexity.

Think small, win big to optimise decision making

Findings from our previous reports relating to company size and R&D productivity continue to hold true. There continues to be a significant negative correlation within the overall cohort of 16 companies between company size (measured by either 10-year R&D spend or revenues) and IRR, along with a positive correlation between company size and cost to bring an asset to market. There are some lessons for large companies in how smaller companies operationalise decision-making that supports more efficient drug development, which we highlight below:

Empower key decision-makers

- Intensive governance processes at larger companies tend to be time- consuming and inefficient. Smaller companies, however, tend to be more nimble with a handful of key decision-makers engaged early to drive programme direction.

Accept risk

- It is common for large companies to focus on de-risking programmes through answering a larger breadth of clinical questions, resulting in longerdevelopment timelines. Smaller companies, by contrast strive to develop strategies to accelerate value demonstration and bring a product to market.

Make quick kills

- Large companies’ risk averse nature means they are not set up to kill projects quickly that no longer meet the minimum success criteria documented in the TPP. Conversely, smaller companies, by answering key questions early and maintaining a keen focus of strategic objectives, are able to make quick kill decisions.

Embed a rigorous but dynamic process to fund projects

- Delays in decision-making due to the aforementioned governance processes can lead to delays in moving programmes forward. Organisations should consider an approach allowing the continuation of programmes between stage gates, focusing governance teams on commercial viability at key decision points.

Staffing and outsourcing: strike the right balance

The decision to make or buy services in R&D is complex, with many influencing factors. Interviewees highlighted that a direct sourcing strategy, covering make-or-buy decisions, is critical. Strategic considerations include: length of time capacity is needed; whether an internal operation or external organisation can be managed effectively; volume volatility and the need for flexibility; maturity of external partners to deliver the required capability; and the degree of control needed over the strategic decision of the capability.

Due to companies providing sub-optimal partner management and maintaining operating models hindering externalisation, many of the contract organisation functions have not yet realised their full potential for delivering efficiencies. Having a clear sourcing strategy, reorganising around process outputs, and relinquishing some control, are all key factors in unlocking potential benefits.

Lifting the burden of data complexity

The data landscape within biopharma R&D is becoming increasingly complex, placing a huge cost burden on organisations. The main challenges are from new technologies, reporting standards, legacy data, external partnerships, siloed inward-facing data architecture, inherited data and systems from M&A deals or in-licensed products. The impact of genomics data, patient generated data from wearables during clinical trials and real world evidence data can be seen as both a big asset for biopharma companies, as well as a considerable liability. Failing to prepare for the problems associated with data complexity could hinder opportunities in the future to take advantage of new data sources.

Our 2016 findings highlight a number of strategies that can be employed by pharmaceutical companies during the development process in order to both improve an asset’s commercial success and drive greater R&D efficiency. Strategies relating to TA focus, product strategy and R&D programme design can all increase an asset’s forecast value, and those relating to governance and decision-making, staffing and outsourcing, and reducing data complexity can all improve R&D efficiency by reducing costs. We consider that the implementation of these strategies will aid companies as they look to balance their own R&D equations.